What Labours new tax policy means for tax rates for investors, trust and businesses

September 14, 2020

Labour has announced that it will increase the top rate of tax for individuals who earn more than $180,000 from 33% to 39%. This will presumably commence on 1 April 2021 for the 2021/22 tax year.

As you know, your PIE funds with us are managed by Mercer. In 2020 Mercer announced their Sustainable Investment Policy, outlining goals for a net-zero emissions investment portfolio by 2050. The Mercer Global ESG (Environmental, Social, Governance) Integration committee meet quarterly to continue to share ideas and collaborate on best practice for sustainable investment. It’s great to know that they have included consulting teams in our backyard – here in the Pacific.

We’re excited to share the following overview of their progress.

Mercer releases their Annual Sustainable Investment Report

Two years into the goal and they are now actively underway. Mercer reports:

“During 2021, we delivered on our policy and portfolio implementation commitments, whilst strengthening our position on climate change by announcing a net-zero by 2050 target for investments managed by Mercer with an expectation to reduce emissions by 45% from 2020 baseline levels by 20301.”

For more details of the highlight report, there is a PDF available for view and download, here.

Two key components to what was achieved in 2021 as a part of the policy

Greater transparency – by launching the first Annual Sustainable Investment Report, and by updating the Task Force about the Climate-related Financial Disclosures document

Commitment to net-zero climate transition – with its implementation now underway as per this report

Why release a Sustainable Investment policy?

Sustainability is one of the key investment beliefs at Mercer and it’s important that we as Managers and Investors understand what this means. Which is why a policy has been created.

In Mercer’s own words, “a sustainable investment approach is more likely to create and preserve long-term investment capital.”

The policy explains that when we talk about sustainability, it doesn’t just incorporate climate change responsibility, but also the responsibility of investment managers to provide clients with a sustainable return on investment and preservation of long-term investment capital.

Mercer’s updated policy for Sustainable investments

In February 2022, the policy was updated to include wording around key implementation developments that occurred during the year, like climate change and UN Global Compact (UNGC).

The updated policy for February 2022 can be viewed, here.

i-Select and your Mercer-managed PIE funds

If you have any questions about our investment offerings and Mercer’s commitment to net-zero carbon investments, please contact one of our team at info@i-select.co.nz

—-----

1 Defined as absolute carbon emissions, per $1M of FUM and Scope 1&2 for the Mercer Investment Trusts New Zealand in aggregate.

Introduction

In 2014 the UK Government indicated its intention to link the retirement age for private pensions to the retirement for the UK State Pension. This followed an incremental increase in the UK State Pension retirement age from 65 so that by 2028 individuals need to be 67 before they qualify.

The age from which private pensions are accessed was increased from age 50 to 55 in 2010, and it is now intended that it will be increased again to 57 from 6 April 2028. Although HMRC are only consulting on this at present, it is almost certain that the rules will be changed.

Anyone born after 6 April 1973 may therefore be affected by this change, possibly delaying their ability to access their UK or ex-UK private pension funds. Advisers will therefore need to take this into account when advising on a transfer of a UK pension to a New Zealand QROPS.

The retirement age for private pensions (the Normal Minimum Pension Age or NMPA) will be preserved for those who are in a pension scheme in February 2021 that gives them a right to take pension benefits before age 57. Moving out of such schemes may result in the loss of this preserved NMPA. Whilst this may not be critical for most people, it is an additional consideration when advising on the appropriateness of a transfer.

Our view is that under the terms of the i-Select Superannuation Scheme, i-Select PIE Superannuation Scheme, and existing SMS schemes, all members as at February 2021 have a right to take pension benefits at an age below 57. As such, they will have their NMPA preserved at 55 beyond the 2028 date. Moving out of one of the schemes, or even between schemes, may result in the loss of this preserved NMPA. Again, it is important to note that this can only affect those born on or after 6 April 1973.

We do not believe we have to change any of our existing trust deeds for this change as the actual or effective NMPA is currently:

i-Select Superannuation scheme: Legacy Members (i.e. those who joined before 01/12/16): their 55th birthday Personal Section Members (i.e. those who joined on or after 01/12/16): Linked to the ability to take benefits under the UK QROPS rules, which is currently 55.

I-Select PIE Superannuation Scheme: Linked to the ability to take benefits under the UK QROPS rules, which is currently 55.

Single Member Schemes: Schemes currently in existence show the age at which benefits can be taken as the member’s 55th birthday.

The NMPA will automatically change for those who joined the scheme after February 2021, and any new SMS schemes created from today will reflect the revised NMPA.

If you have any queries regarding this, please let us know.

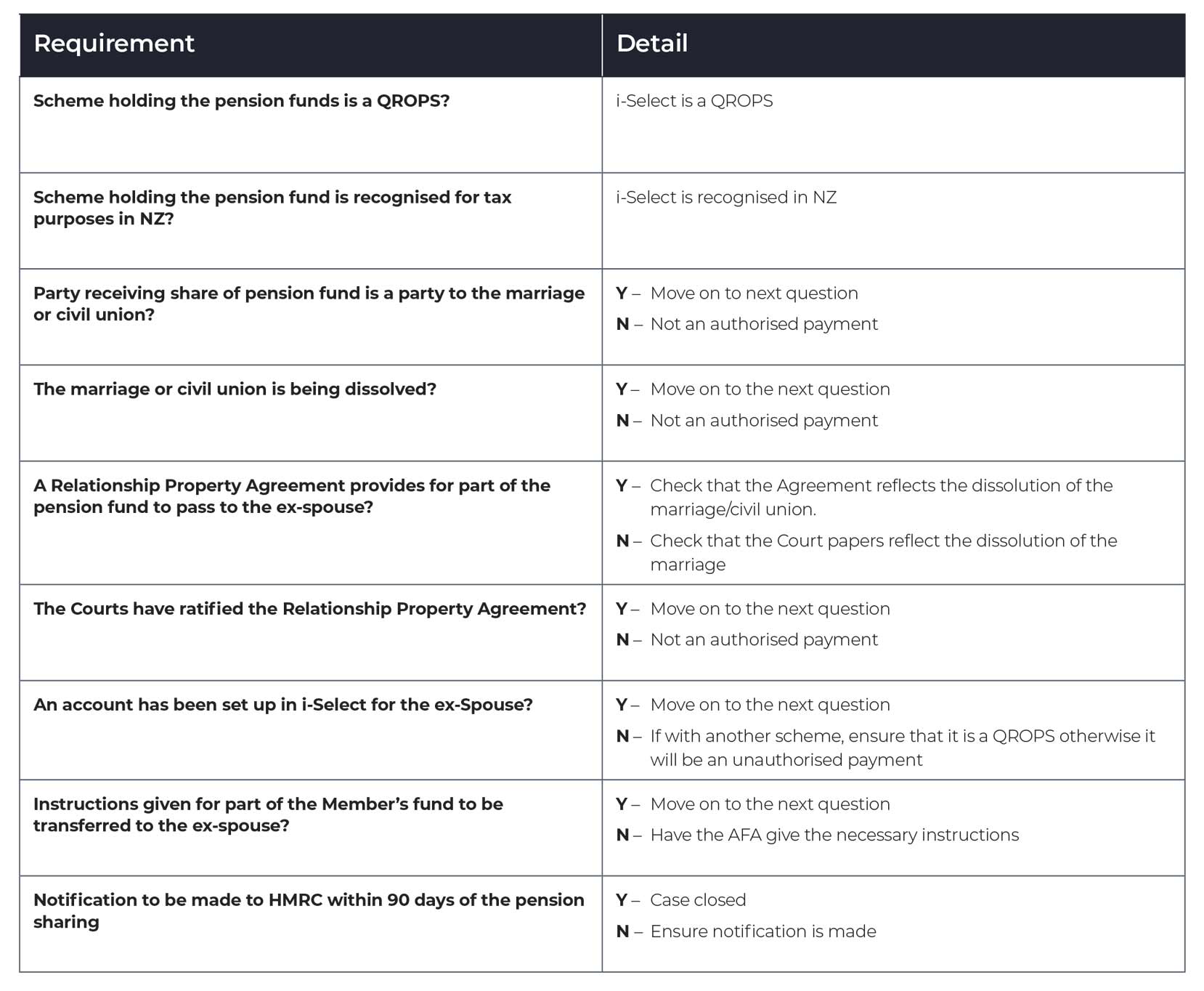

Background

If part of a pension within a QROPS that originally derived from a UK pension is transferred to an ex-spouse as part of a separation, it will be classed as an unauthorised payment unless it is done in accordance with UK pension sharing rules. An unauthorised payment will result in a charge being levied on the Member of up to 55% of the value of the transfer to the ex-spouse. Such charges are not prevented by the UK/New Zealand Double Taxation Agreement as it is not considered to be a tax and is therefore outside the ambit of such an agreement.

UK Regulations applicable to QROPS

The pension sharing regulations in the UK were extended in 2006 to cover overseas pension schemes by The Pension Schemes (Application of UK Provisions of Relevant Non-UK Schemes) Regulations – SI 2006/07).

This regulation applies to the division of a fund within a QROPS on the dissolution of a marriage, which includes a civil partnership, but not a de-facto partnership.

The requirements for a pension split to be an authorised payment under the UK regulations are as follows:

The pension splitting scheme must be a ROPS;

It must be recognised for tax purposes in the country in which it is situated;

The relationship must be a marriage or civil partnership;

The ex-spouse receiving a share of the pension fund must have been a party to the marriage;

The pension sharing order must be in the form of an order of a court in connection with proceedings relating to the dissolution of the marriage or civil union.

The share of the pension fund passing to the ex-spouse must be to a QROPS. It does not need to be a different QROPS scheme.

Under New Zealand law, pension sharing can be achieved with just a Relationship Property Agreement validly executed under the Property (Relationships) Act 1976. This does not require the marriage to be dissolved, and it does not require the courts to be involved. However, the UK regulations require the pension sharing to have been both by order of a court and in relation to proceedings that will lead to the dissolution of the marriage or civil union.

Suggested clause

An example agreement to be put to the Courts to be used as part of the application to the Courts for ratification of a Relationship Property Agreement is attached. This needs to be considered by a lawyer.

Checklist

A checklist of the requirements is as follows:

Introduction

This report is intended to supplement the information provided directly by an individual who is intending to transfer their UK defined benefit or guaranteed annuity rate pension funds to a New Zealand QROPS.

It is divided into:

The New Zealand tax treatment of foreign pension schemes owned by New Zealand tax resident individuals;

The New Zealand tax treatment of benefits received from foreign pension schemes by New Zealand tax resident individuals;

The New Zealand tax treatment of transfers of foreign pension funds to New Zealand superannuation schemes by New Zealand tax resident individuals; and

General information about New Zealand’s tax system as it relates to New Zealand superannuation schemes for New Zealand tax resident individuals.

Pensions and pension schemes are colloquially known in New Zealand as superannuation and superannuation schemes. The two are interchangeable, and here I use both.

For New Zealand tax purposes, UK pension schemes are in the same category as all overseas pension schemes, but I use the phrase overseas pension scheme and UK pension scheme interchangeably here.

1. NZ tax treatment of foreign pension schemes

The income or gains of foreign pension schemes have ceased to be annually taxable on individuals in NZ from 1 April 2014. Before that date, subject to a number of complex exemptions, individuals were technically taxable on the growth in value of their overseas pension fund each year.

From 1 April 2014, individuals became taxable on a notional amount of income calculated when they make lump sum withdrawals. Withdrawals are defined as the transfer of an overseas pension fund to a New Zealand scheme as well as the taking of benefits directly from the overseas scheme.

Under the new rules, transfers between foreign superannuation schemes is not taxable for a New Zealand tax resident provided the transfer is not to an Australian pension scheme. Transfers to Australian schemes are outside of this rollover provision because transfers from Australian superannuation schemes to New Zealand schemes are exempt from New Zealand taxation.

When the rules were introduced in 2014, they were made retrospective, and the old rules were grandfathered. This means that any individuals that transferred their UK pensions after 31 March 2014 who had not applied the ‘old’ rules, prior to that were required to adopt the new rules as if they had applied at all times. Any individuals who had correctly and consistently applied the old rules could opt to continue using the old rules if doing so was to their advantage.

2. NZ tax treatment of benefits from foreign pension schemes

2.1 The rules if no exemptions apply

Pension income is taxable in full on a receipts-basis, which means that it is taxable in the tax year in which it is received. The word ‘pension’ is not defined in tax legislation, so it takes its ordinary meaning of being income received on a regular basis from a retirement savings scheme. Any annuity, regular drawdown, or defined benefit pension that is not a lump sum will therefore fall into this category.

A withdrawal from a foreign superannuation scheme that is not a pension (i.e. it is a lump sum) is taxed in a more complex way. The rules that apply were introduced with effect from 1 April 2014 and involve determining:

When it applies: It applies when there is a:

Lump sum withdrawal

Transfer to New Zealand

Transfer to Australia

Transfer of an interest to another person

When it does not apply: It does not apply to:

Transfers of interests under formal relationship property agreements (a formal legal process between couples that does not necessarily involve divorce)

Withdrawals within a specified period of exemption

Withdrawal amounts in excess of the amounts calculated using one of the two permitted methods

The Exemption period: This is usually the month of arrival and the following 48 months.

The Assessable Period: This is generally the period between the end of the Exemption Period and the derivation of the withdrawal.

The methods permitted to calculate the assessable amount: The two methods are:

The Schedule Method

The Formula Method

2.2 Exemption period

The exemption period starts when a person first becomes tax resident after they first join a foreign pension scheme and applies for the month of arrival and the following 48-month period. This exemption period can end before the expiry of 48 months if a person becomes non-resident. A person may only have one exemption period.

2.3 Assessable period

An assessable period follows an exemption period, and each tax year that passes tends to increase the amount of notional assessable income that a person must declare and pay tax on if they take a lump sum withdrawal.

Any period of non-residence is not part of an assessable period. For example, if a person joined a UK pension scheme, came to NZ for three years, became non-resident for another five years before returning again, they would effectively have an 8-year exempt/non-assessable period.

2.4 Schedule Method of calculating income

The Schedule Method is the default method of calculation and may be used for defined contribution schemes, but is compulsory for defined benefit schemes. In its simplest form, it requires an individual to count the number of tax years that have started between the end of an exemption period and the foreign superannuation withdrawal (with a minimum of 1). The number derived determines the percentage of the withdrawal that is taxable and is called the Schedule Year Fraction. The more years collected, the greater the percentage of the fund that is taxable.

The Schedule percentages are:

2.5 Formula Method of calculating income

The Formula Method of calculation may be used for a withdrawal from a defined contribution scheme but cannot be used for a withdrawal from a defined benefit scheme.

A brief description is therefore included here only for completeness. The method requires a calculation of the increase in value of a pension fund from the end of any exemption period to the date of withdrawal. The raw gain is then put through a formula which increases the gain by a factor dependent upon the length of time it has accrued without NZ taxation being charged. If a pension scheme has decreased in value over this period (e.g. because of exchange rate movements) the income is zero.

The logic for this method not being permitted for interests in defined benefit schemes is that the market value at the date of the commencement of the assessable period is unlikely to be readily available. In some instances, however, the market value at the relevant date has been calculated by an actuary and has been used as a basis to consider transferring a defined benefit interest to a SIPP prior to a transfer to a New Zealand scheme. This would permit the use of the Formula Method, but may be subject to Inland Revenue Department (IRD) scrutiny.

2.6 Lump sums from defined benefit schemes

The IRD’s view is that lump sums taken from defined benefit schemes that involve a commutation of an entitlement to income are fully taxable rather than taxable under the rules associated with lump sum withdrawals. The rationale for this is that the lump sum is an advance of income resulting from an option exercised by an individual, not a withdrawal of a capital amount. The form of the payment (i.e. a lump sum) does not change the nature of the payment for New Zealand tax purposes (i.e. it is, and remains, taxable income). An important requirement for this legal principle to apply is that, following the lump sum payment, a pension must commence or continue. There is New Zealand and overseas (including Australian and UK) case law to support this legal position.

Where scheme rules provide for the payment of a non-optional lump sum on the commencement of a pension, the lump sum withdrawal rules would apply to the member’s entitlement, and it would not be treated as income.

2.7 Transitional Residence

There is a separate overriding exemption from NZ tax given to new tax residents and to returning residents if they have been tax-resident outside of New Zealand for at least 10 years. This is called Transitional Residence, and it generally results in all foreign passive income being exempt from New Zealand tax for the month of arrival and the following 48 months. Passive income includes interest, dividends, pension payments or withdrawals, rents, and royalties. Any lump sum or regular income benefits from UK pension schemes received in this period are therefore exempt from tax, as are the transfer of any UK pension funds to NZ schemes.

2.8 Summary

In summary:

The receipt of a pension from a UK pension scheme is fully taxable.

Lump sums payments that derive from an option to commute part of a defined benefit pension will retain their income nature and will be fully taxable as income in New Zealand.

Outside of any period of exemption related solely to foreign pension schemes, the receipt of a lump sum withdrawal from a UK pension scheme may be partly or fully taxable, dependent upon the length of New Zealand tax residence, with the amount determined by one of two methods.

Any pension payments or lump sum withdrawals from a foreign pension scheme during a period of Transitional Residence is exempt from NZ tax.

3. Taxation of lump sum transfers to New Zealand Superannuation schemes

Transfers are treated in the same way as lump sum withdrawals. Accordingly, exemptions, exemption periods, assessable periods and the Schedule and Formula methods apply in the same way.

The transfer of a defined benefit pension fund in payment would be treated as a capital lump sum to which the Schedule Method of income calculation would apply. This is on the basis (as outlined in 2.6) that there would be no ongoing pension payments following the pension transfer.

4. General information about New Zealand’s tax system

Tax Year

The New Zealand tax year runs from 1 April to 31 March each year.

Personal allowances

There are no personal allowances in New Zealand

Personal tax rates

Personal tax rates are progressive, and the tax bands are:

$0 to $14,000 - 10.5%

$14,001 to $48,000 - 17.5%

$48,001 to $70,000 - 30%

$70,000 + - 33%

Capital taxes

There are no capital taxes in New Zealand. This includes:

Capital gains taxes;

Gift taxes;

Inheritance taxes

However, where capital gains are considered to have the nature of income in specified ways, the income tax legislation provides for gains to be taxed as income.

Tax reliefs

Expenditure incurred in order to generate assessable income is generally deductible for tax purposes, but there are few tax incentives that relate to investments or savings. In particular, there are no tax reliefs for personal pension contributions, but the antithesis of this is that benefit payments from New Zealand superannuation schemes are not taxed on individuals.

Superannuation Schemes in New Zealand

In broad terms, for tax purposes, superannuation schemes in New Zealand can be categorised as:

Portfolio Investment Entities (commonly abbreviated to PIEs); or

Non-PIE but widely held; or

Non-PIE and not widely held.

A PIE is a unitised investment vehicle that attributes income and gains to individual investors for the purpose of applying tax rates nominated by individuals that must reflect their personal marginal rates of tax. This is designed to remove the tax disadvantage that low earning taxpayers otherwise face when investing in investment vehicles with higher tax rates. The tax rates that investors can nominate (the Prescribed Investor Rate, or PIR) are:

Tax Year

The New Zealand tax year runs from 1 April to 31 March each year.

Personal allowances

There are no personal allowances in New Zealand

Personal tax rates

Personal tax rates are progressive, and the tax bands are:

Tax reliefs

Expenditure incurred in order to generate assessable income is generally deductible for tax purposes, but there are few tax incentives that relate to investments or savings. In particular, there are no tax reliefs for personal pension contributions, but the antithesis of this is that benefit payments from New Zealand superannuation schemes are not taxed on individuals.

Superannuation Schemes in New Zealand

In broad terms, for tax purposes, superannuation schemes in New Zealand can be categorised as:

Portfolio Investment Entities (commonly abbreviated to PIEs); or

Non-PIE but widely held; or

Non-PIE and not widely held.

A PIE is a unitised investment vehicle that attributes income and gains to individual investors for the purpose of applying tax rates nominated by individuals that must reflect their personal marginal rates of tax. This is designed to remove the tax disadvantage that low earning taxpayers otherwise face when investing in investment vehicles with higher tax rates. The tax rates that investors can nominate (the Prescribed Investor Rate, or PIR) are:

Resident investors:

10.5% for those with taxable income up to $14,000 provided their non-PIE and PIE income combined is less than $48,000.

17.5% for those with taxable income between $14,000 and $48,000 provided their non-PIE and PIE income combined is less than $70,000.

28% where an investor does not qualify for rates of 10.5% or 17.5%.

Non-resident investors

0% where the PIE scheme invests mainly in foreign investments and has formally elected to be a Foreign Investment PIE, and the investor qualifies as being a Notified Foreign Investor.

28% where the investor does not qualify for the 0% PIR

Widely held superannuation schemes that are not PIEs are taxed at a flat rate of 28%. To be a widely held superannuation scheme, it must have, or must anticipate having, over 20 investors.

A non-widely held, non-PIE superannuation scheme is taxed at a flat rate of 33%.

Payments out of superannuation schemes

Payments of benefits made by New Zealand superannuation schemes are not liable to New Zealand tax in the hands of residents and non-residents alike. This is on the basis that individuals have not had New Zealand tax relief on the contributions to the schemes, and the New Zealand superannuation fund has been taxed on its income in the growth phase.

Introduction

The purpose of this brief article is to explain how taxation works within the i-Select Superannuation Scheme (Scheme).

Trust tax

The Scheme is set up as a trust and pays tax in the same way as a trust. Every trust has a trustee, who looks after the assets, collects the income, and pays the bills. They are also the trust’s single taxpayer and it is their responsibility to work out the taxable income, complete a tax return, and pay any tax liability arising.

A beneficiary is a person who will ultimately benefit from the trust’s assets and income, but before they do, they must rely on the trustee to deal with all of the trust’s affairs on their behalf. They therefore have no responsibility to collect income, work out the trust’s tax liabilities, report them, or pay them.

In the i-Select Superannuation Scheme, Public Trust is the Trustee, and i-Select Ltd (i-Select) is the Manager. It is the responsibility of i-Select, on behalf of Public Trust, to do all of the income tax calculations, complete the tax return, and organize the payment of any necessary tax.

How Trust tax affects Members

This is why members of the scheme do not have to put any of the income arising from their portfolio within the Scheme onto their tax return. Essentially it is not their taxable income, it is the trustee’s, and if they put any scheme income on their tax return it will result in a double charge to tax.

Scheme tax

We calculate the tax position of the Scheme for a year by collating all of the tax reports for each of the members’ portfolios within the scheme at the end of the tax year. The taxable income of the scheme is generally made up of income that is fully taxed, income that is not fully taxed and the Scheme’s expenses.

Income that is fully taxed includes things like New Zealand interest and dividends and Portfolio Investment Entity (PIE) income. Income that is not fully taxed is mainly foreign interest, foreign investment fund (FIF) income, and currency gains and losses. The expenses of the Scheme include the fees of i-Select (which pays many of the scheme’s expenses) and advisers.

Most of the Scheme’s tax liabilities are therefore paid at source, leaving only the untaxed income and the expenses. In any given year, this will either produce a net amount of taxable income, or a net loss. Where it produces a loss, the Scheme receives tax refunds and may have losses to carry forward. Where it produces income, it will either consume losses or will result in an overall tax liability that must be paid directly.

On the one hand, the vast majority of FIF income can be reasonably estimated at the start of the year as it depends upon the value of FIFs held on the first day of the year. On the other hand, currency gains or losses in many cases will not be capable of calculation until the end of the tax year, as it depends upon the exchange rate on the last day of the year, 31 March.

The Scheme’s tax rate is 28% (as opposed to a family trust’s rate of 33%) as it qualifies as a widely held superannuation scheme.

How Scheme tax affects Members

On an individual basis, every member’s portfolio has a share of the Scheme’s income and deductions each year, which may produce taxable income, or a tax loss, and will contribute proportionately to the Scheme’s overall tax position. Regardless of whether the Scheme has an overall tax liability or is due a refund, within the membership at any one time there will be members with liabilities and members with losses. Here’s a simple illustration of this:

1,000 members with total tax liabilities of - $1,000,000

400 members with losses reducing the tax liability by - $250,000

The Scheme’s overall tax liability would be: - $750,000

Each member will also have tax credits of some sort (e.g. Resident Withholding Tax, Imputation Credits, or foreign tax) which may mean that direct tax payments are not required. Using the above example:

The Scheme’s overall tax liability would be: - $750,000

Total tax credits on income - $800,000

Net refund to the Scheme - $50,000

In this way, a person with a tax liability may not be called on to settle their share of the liability immediately because other member’s losses and tax credits have deferred the need to make direct tax payments. At some future date when the Scheme’s tax position makes it necessary to make a direct tax payment to the IRD, then we may require a full or partial payment of a member’s share of the Scheme’s taxes. In the interim, they enjoy a tax deferral.

On the other hand, if a member takes full benefits, or if they transfer out of the Scheme, then full payment of tax liabilities is required, and this can cover a number of years of tax liabilities and can be large or small.

In order that members know their tax position each year, we prepare an annual report in which we set out their accrued tax position. This will make clear what tax liabilities have been deferred in the manner described above.

Tax is tricky enough when it comes to bringing pensions over to New Zealand, but there may be some new pitfalls. Here are some of our recommendations, base on what we know at this stage.

1. Transfer sooner rather than later

It may be wise to consider transferring UK pensions sooner rather than later. Many transfers produce a notional amount of income that is substantial. Added to high taxable income levels, this notional income may suffer tax at 39% in2021/12 rather than 33% in 2020/21.

For example, $250,000 transferred in 2020/21 generating 27.47% income after 10years of residence (i.e. $68,675) will generate a maximum tax liability of$22,663 at 33%. In 2021/22 the same transfer will generate income at 31.80%, or$79,500 (because of the extra year of residence), and a maximum tax liability of $31,005 at 39%

2. Don’t take maximum benefits

There are more variables involved than just tax but, simply put, it may not make sense to take full benefit withdrawals from QROPS superannuation schemes solely in order to avoid the management charges within the managed investment scheme. From the time that the funds are extracted, the income from the released funds may be exposed to a maximum rate of tax of 39% compared to a scheme rate of 28%.

For example, $250,000 earning income of 5% within the i-Select scheme will generate net income (after management charges) of $11,350 and will suffer tax of $3,178at 28%. The net income will be $8,172. That same income earned personally but without management charges will produce taxable income of $12,500 which may suffer tax of $4,875 at a top rate of 39% giving a net return of $7,625. This represents a tax differential of $547.

Other possible impacts

Withdrawals from KiwiSaver and other investment entities with a maximum income tax rate of 28% may decrease in order to shield investment returns at a lower tax rate.

Salaries may reduce, leading to reduced borrowing capacity, or requiring banks to re-adjust to differing income sources in their lending criteria.

Investment trends may change with an increasing emphasis on realising capital gains. This may result in a concentration on the property market.

Expenses that are tax deductible may again change behaviour with interest deductions being maximised and shifted to salary-earning individuals.

Labour has announced that it will increase the top rate of tax for individuals who earn more than $180,000 from 33% to 39%.This will presumably commence on 1 April 2021 for the 2021/22 tax year.

They have committed to “no new taxes and no further income tax changes for at least the next three years”.

Tax rate planning or tax avoidance?

When the top rate of tax was last at 39%, starting at $70,000, the number of individuals coincidentally earning $70,000 or just below was rather incredible. Profits above this figure were extracted from companies in a variety of ways, using dividends and interest often paid to a trust for tax-efficient distribution.The rate was also high enough to spawn a number of tax avoidance schemes and engage considerable IRD resources in this area.

Whilst it is permissible to structure your affairs how you wish, the IRD has the power to ignore a tax avoidance arrangement and undermine any actions that reduce tax.An avoidance arrangement is something that directly or indirectly has tax avoidance as its objective or one of its objectives, or has the effect of tax avoidance. Any tax rate planning undertaken following the introduction of a 39% tax band should therefore bear this in mind, and professional tax advice is recommended.

Planning

Depending upon whether Labour stick to the letter of their policy and make no other changes to tax laws, and taking into account the risk of it being considered tax avoidance, those with incomes over $180,000 could consider:

• In conjunction with estate and risk planning, share movements from personal names to trust in order to distribute dividend income tax-effectively to beneficiaries, taking account of:

Continuity for imputation credits

Continuity for losses

Interest relief for loans to purchase shares

• As part of retirement planning, the payment of superannuation contributions to:

KiwiSaver schemes

Superannuation scheme

Unregistered superannuation schemes

• With a view to enhancing or simplifying their lifestyle or reflecting their private or business use of assets and services, the conversion of salary to fringe benefits

Bear in mind that the IRD may be watching for this kind of activity with a view to re-activating their anti-avoidance programmes. Back in 2009 they were emboldened by the successful prosecution of the Penny & Hooper tax-avoidance case before it was rendered superfluous by tax rate harmonisation.

The devil will be in the detail of Labour’s policy, because if you took them at their word (“… and no further income tax changes”) you would have to wonder what this means for the following tax rates:

PIE tax rates

PIEs were introduced in 2007 and the top PIR (Prescribed Investor Rate) was 30%. This was reduced to 28% in 2009 in order to align with the top rate of tax for companies and thereby remove any tax differences between the two entities. This was part of a tax rate alignment following the reduction of the top personal tax rates from 39% to 33% in 2009.

If the topPIR stays at 28%, it will represent a significant tax advantage to savers with taxable income of more than $180,000. For KiwiSaver schemes, on the one hand it is likely that salaries will start to reduce to below $180,000 to save tax and thereby decrease the amount of employer and employee contributions. On the other hand, depending upon the rate of ESCT (see below), it could see increased employer-only contributions via salary sacrifice.

The ESCT (Employer Superannuation Contribution Tax) and RSCT (Retirement Savings Contribution Tax) tax rates

The top rate of ESCT (formerly called SSCWT) and RSCT was decreased from 39% to 33% in 2009in line with the reduction in the top rate of income tax.

If the top rate of ESCT and RSCT remain at 33%, it will represent a significant tax advantage for remuneration to be paid as contributions to superannuation orKiwiSaver schemes as:

· Profit will be extracted from the company net of 28% tax

· Income and gains within the superannuation scheme will be taxed at 28%

· Benefits can be taken from the scheme without tax applying.

This may result in the return of salary sacrifice with a corresponding increase in the number of tax avoidance cases pursued by the IRD.

FBT tax rates

The top FBT tax rate was decreased from 63.93% to 49.25% in 2009 in line with the top rates of personal tax. The top rate of 49.25% is the top rate of personal income tax(33%) grossed up.

If the top rate of FBT remains at 49.25%, it will mean that being remunerated by fringe benefits (e.g. cars, goods and services) will be tax efficient.

Company tax rates

Company tax rates decreased from 33% to 28% over a period of years between 2009 and 2011 to make them internationally competitive.

If the company rate remains at 28% there will be considerable incentive to retain profits within companies where the shareholders can afford to do this. Profits may then be extracted in more tax-effective ways other than salary (e.g. fringe benefits, superannuation contributions or dividends to lower tax-rate individuals or entities such as trusts).

Trust tax rates

The trust rate of tax has consistently been 33%. When the top rate of personal tax was39% there was considerable amount of arbitrage with trusts, with company shares owned by trustees and dividends distributed to low earning spouses, non-minor children, or simply converted to capital in order to permanently remove the additional 6% of income tax.

If the trust rate of tax remains at 33% this structuring and activity will return, with shares transferred to trusts, salaries reduced, and dividend payments increased. It may also lead to the maximisation of dividends payments to trusts in order to increase trustees’ loan accounts within companies on which interest will be charged, again extracting income from companies at a maximum tax rate of 33%.

Take the next step...

Let us help you decide the best way to transfer and manage your superannuation, or help you navigate the tax issues involved in bringing your pension into New Zealand.

All writers' opinions are their own and do not constitute financial advice in any way whatsoever. i-Select strongly recommends that you perform your own independent research and/or speak with a qualified financial advisor before making any financial or tax decision.